By Gerry Rodriguez

Sportradar (Nasdaq: SRAD) is set for a strong Q2, fueled by major sporting events like UEFA EURO 2024 and the ATP, with expected revenue surpassing Q1’s €266 million. The company’s innovative products, revenue share model, and key hires in technology are driving growth, leading analysts to project a target stock price of $22.91, well above the current $11.07. Sportradar is poised for long-term success in the expanding sports betting market.

Key Insights

- Increased interest and solid margins across EURO 2024 and Indian Premier League key to underestimated profits for SRAD with their revenue share model

- Huge volume of ATP matches and new products to power revenues versus 2023

- Robust business model to take advantage of tailwinds in Brazil

- Two key hires are expected to have immediate impact

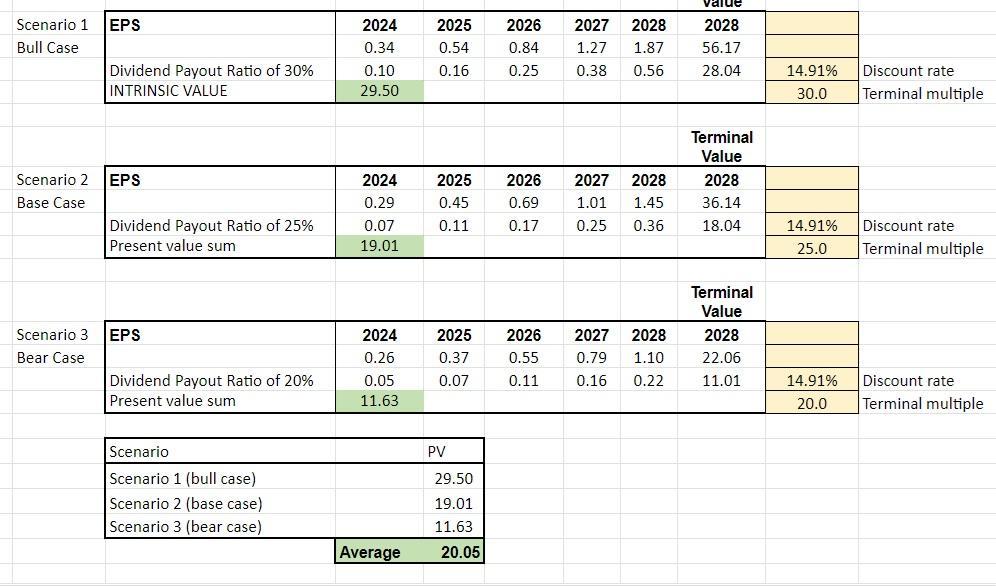

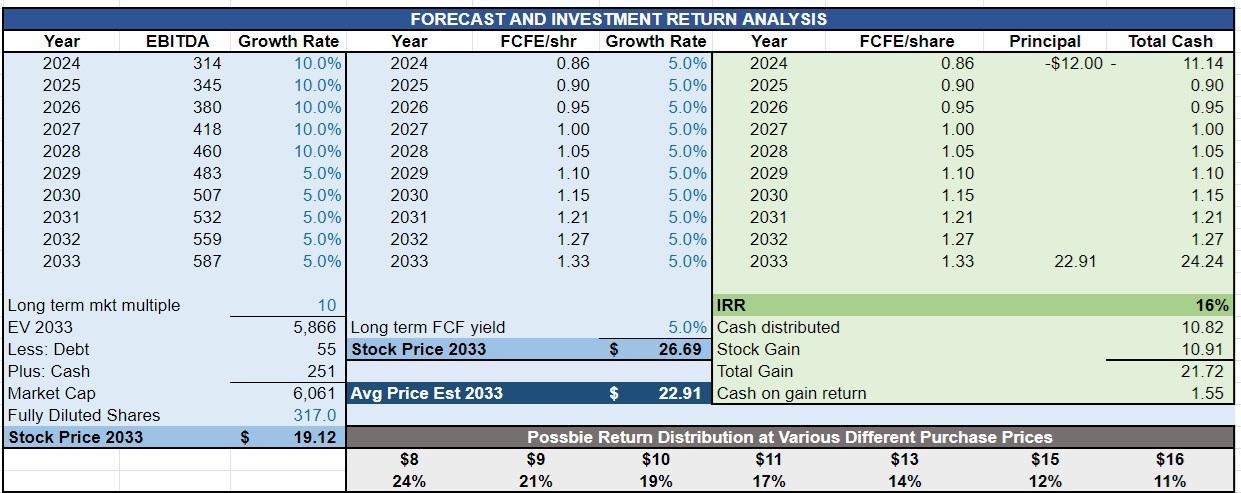

- DCF model shows $22.91 target stock price vs. current $11.07

Revenue Soaring

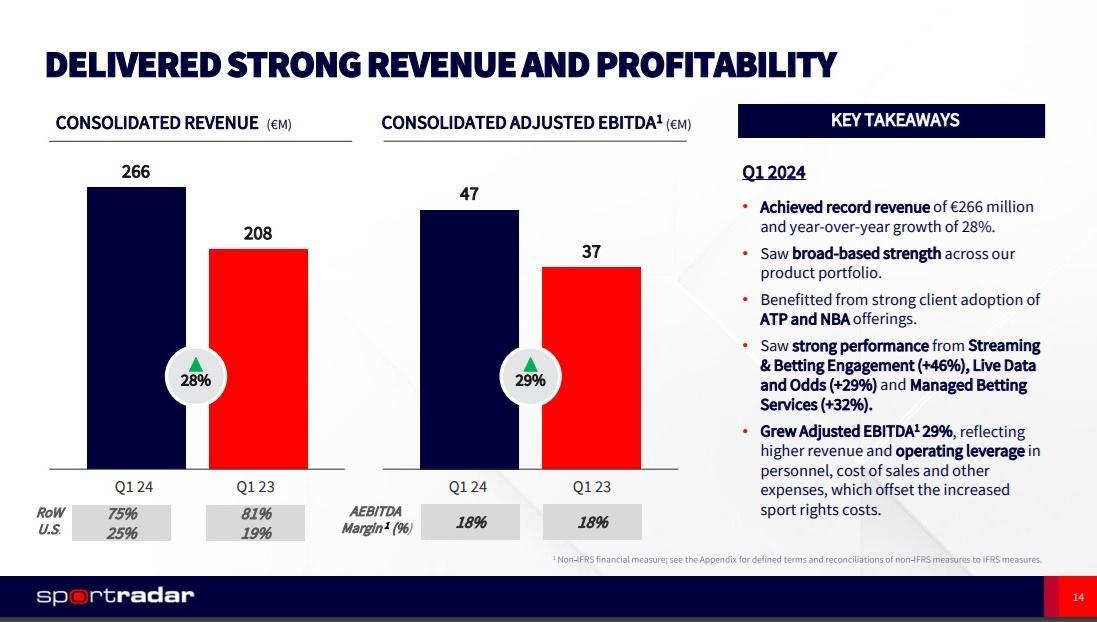

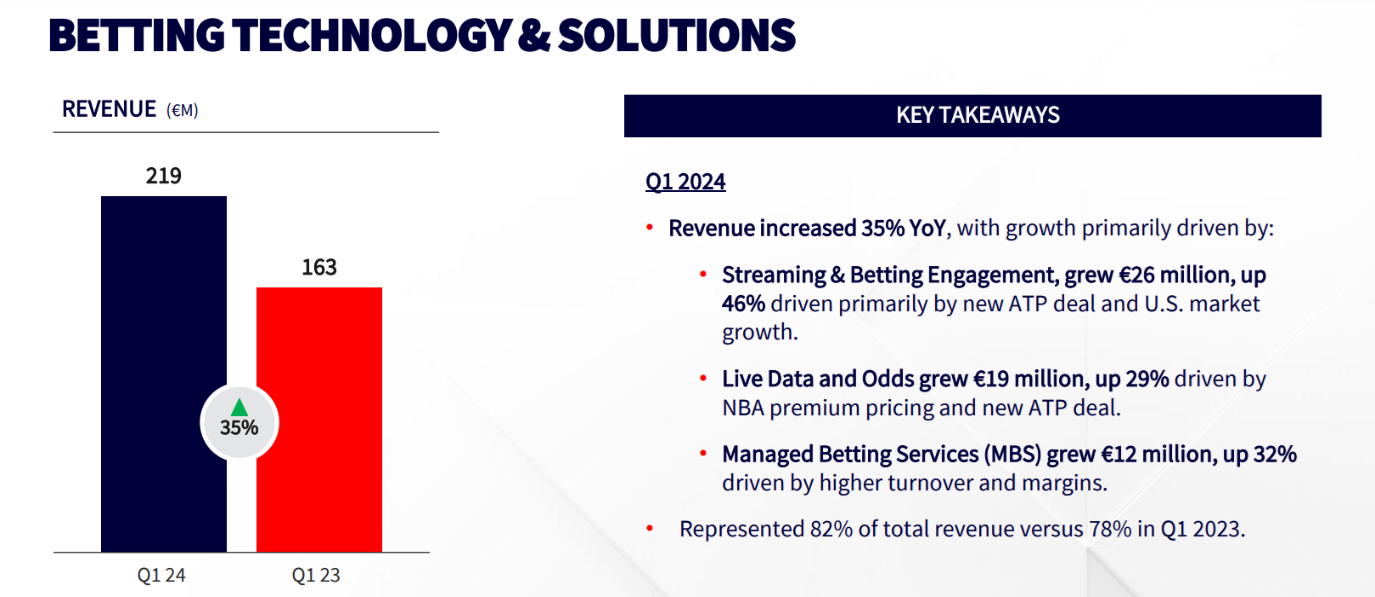

Every shareholder of large bookmakers such as DraftKings (Nasdaq: DKNG) knows to look out for seasonal revenues relating to the Superbowl or Stanley Cup Finals. But SRAD – which delivered €266m 2024 Q1 revenues and “Betting Technology & Solutions” 2024 Q1 revenue of €219m – is in fact tied to the growth of sports betting globally.

SRAD Q1 2024 Earnings Presentation: https://investors.sportradar.com

SRAD Q1 2024 Earnings Presentation: https://investors.sportradar.com

There was very encouraging news for investors in Q1 with 28% YoY growth across the business and an eye-opening 35% YoY increase for the Betting Technology & Solutions vertical. This is somewhat close to DKNG’s 53% as per their Q1 2024 earnings. The latter is able to increase off the back of expensive customer acquisition and marketing which led to a repeated net loss in Q1 of $143m. This is in stark comparison to SRAD’s 19% Adjusted EBITDA margin and a 2023 net profit margin of 3% or €7m, and €275 million cash and cash equivalents / €220 million undrawn credit facility, compared to €460 million in Q1 2023.

Having established Q1 was a rip-roaring success, what is expected in Q2?

Revenue in the second quarter of 2023 increased 22% to €216.4 million compared with the second quarter of 2022 and above Q1’s figure of €208m. Therefore, we can expect 2024’s Q2 to be slightly higher than Q1’s €266m. But, there are a number of sporting events which could drive these revenues higher:

- EURO 2024 – Darren Small, SVP of Managed Trading Services said the following in an interview after the tournament finished:

“Overall, the tournament was good for us. We saw a very low-scoring tournament, particularly from some of the most favoured teams. I don’t even think France managed to average a whole goal out of the games. I think they averaged around 0.67 goals a game. The same thing with Cristiano Ronaldo not scoring many goals in open play. In fact, from a betting perspective, they probably were the two of the heaviest-backed teams and individual top goal scorers in the competition.”

These figures may not have been taken into account by investors as SRAD’s Managed Trading Services are overlooked in favour of their traditional subscription service data products.

- Indian Premier League (cricket) & Cricket World Cup – there is reason to believe SRAD over-performed versus expectations.

LinkedIn: Link

In addition to the Indian Premier League, the Cricket World Cup featured an exciting contest and whilst favourites India prevailed, there is sure to have been betting profits made.

- ATP – SRAD’s jewel in the crown is going to bring new revenue versus 2023, having won the rights from competitor IMG Arena late last year. What’s even more encouraging is the products which have been built to complement the comprehensive betting coverage. In March 2024, SRAD launched 4Sight. According to SRAD:

“In essence, the technology overlays ultra-fast data into live streams, delivering a continuous flow of engaging statistics that appear in real time, from serve speed and ball bounces, to total shots in each rally.”

- WNBA – and what about superstar Caitlin Clark, driving incremental revenues via SRAD’s NBA partnership? How could we forget this 10 year partnership and even embedding betting solutions within NBA’s League Pass.

With Q2 revenues likely secured off the back of significant rights deals and good performance in marquee tournaments, let us turn our attention to personnel.

Wise Heads

In May, SRAD announced two significant additions to its roster – CFO Craig Felenstein and Chief Technology and Artificial Intelligence Office Behshad Behzadi.

SRAD Q1 2024 Earnings Presentation: https://investors.sportradar.com

These hires signal both a maturity and an investment in the future. Both are expected to create immediate value in terms of SRAD’s business model and galvanising the company to think BIG.

This comes off the back of restructuring in January:

“By centralizing our key business functions, we will foster greater collaboration and faster decision making, enabling us to drive further operating efficiencies and increased innovation across our business,” Sportradar CEO Carsten Koerl said in a statement. “These decisive steps will enable us to better serve our clients and partners as well as capture the significant market opportunities ahead of us.”

With SRAD relying on both its People, sporting tailwinds, its technology and a nod to AI, the future is certainly bright.

DCF Model

Based on all available information, we are able to build a DCF model, reflecting the historical and continued growth in revenue and EBITDA for SRAD.

SRAD DCF model – EPS by analyst DC

SRAD DCF model – stock price output by analyst DC

For Sportradar, net margins are rising quickly from a low point and could benefit from a number of factors, not least of which is the current summer’s schedule of important sporting events. Given the rapid expansion of the US betting market, the firm is especially well-positioned to take a larger portion of this market. Sportradar’s leading position in the rapidly expanding sports betting business makes us think that the management team’s expectations of double-digit revenue CAGR through the end of the decade—driven by market expansion, new markets, new products, and improved product penetration—are realistic. In addition, we think that when Sportradar grows in the US, EBITDA margins will probably rise from 20% to 25%.

All things considered, we think Sportradar provides investors with long-term exposure to the quickly expanding sports betting market with a pure-play potential through a successful B2B operating model that is mostly subscription-based (around 76% of revenue). With a 20% two-year adjusted EBITDA CAGR, a robust balance sheet (with $240 million in cash versus debt and 98% equity as a percentage of total capital), $200 million in planned share repurchases for 2024, increased operating leverage in subsequent years, and a fair valuation in light of its growth prospects and comparable companies, the company has one of the strongest growth profiles in its industry.

Conclusion

We have a stock that is undervalued and misunderstood. We predict a lucrative Q2 driven by SRAD’s betting revenue share sales model, restructuring of the business in Q1 and a very resistant business with a significant moat for future years.

Links:

Disclaimer: The views, suggestions, and opinions expressed here are the sole responsibility of the experts. No State Today USA journalist was involved in the writing and production of this article.